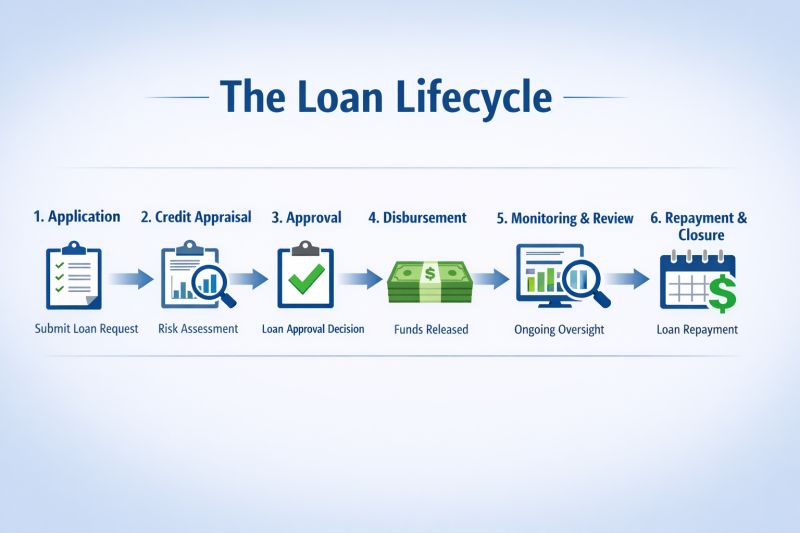

The End-to-End Loan Lifecycle: How R2S FinCore Powers Modern Lending, From Lead to Closure

Ask most people what a loan journey looks like, and they'll describe two moments: filling out an application, and money hitting their account. In reality, between those two moments lies a complex, tightly choreographed sequence of systems, teams, and decision engines — each one responsible for reducing risk, ensuring compliance, and protecting both the lender and the borrower.

At R2S FinCore, we built our Lending Management platform around this reality. Rather than treating loan origination and loan servicing as separate problems, R2S Fincore connects the entire lifecycle — CRM, LOS, LMS, Collections, Credit Risk, and Compliance — into a single, intelligent ecosystem. Here's what that journey actually looks like, stage by stage.

1. Lead Sourcing

Every loan starts as an opportunity, and opportunities can come from anywhere: DSAs, branch walk-ins, digital channels, partner networks, referrals, or targeted campaigns. A modern lending platform needs to capture leads from all these sources without losing context — because the channel a lead comes from often shapes how it should be qualified and served.

2. CRM: Turning Leads Into Relationships

Once a lead enters the system, the CRM layer takes over. This is where a lead is created, assigned to a relationship manager, and nurtured through customer interaction. Qualification happens here too — separating genuine intent from noise before any operational cost is spent on processing.

3. Opportunity Creation

A qualified lead becomes an opportunity, and that opportunity is formally handed off to the Loan Origination System (LOS) for processing. This handoff is a critical control point: it's where sales-side engagement becomes a structured, auditable application.

4. Loan Origination System (LOS)

This is where the real underwriting groundwork begins. The LOS manages application creation, bureau checks (CIBIL and other credit bureaus), deduplication to catch duplicate or fraudulent applications, pre-screening against eligibility norms, and integration with external APIs for data enrichment. It's the engine room of the front-end lending process — fast, but never careless.

5. Verification Layer

Before any credit decision is made, the facts on the application need to be independently verified. This layer includes:

- Field Investigation (FI) — confirming addresses, employment, and business details on the ground

- Risk Containment Unit (RCU) — screening for fraud indicators and inconsistencies

- Legal Verification — validating ownership and legal standing of collateral or property

- Technical Verification — assessing the physical and technical soundness of an asset

Verification is where trust is built into the file — it's the difference between a decision based on claims and a decision based on evidence.

6. Credit Assessment

With verified data in hand, credit assessment brings together eligibility calculation, scorecard evaluation, deviation management for exceptions, and preparation of the Credit Appraisal Memo (CAM). This is the analytical heart of the lending process — where policy, risk appetite, and individual borrower circumstances are weighed against each other.

7. Underwriting & Approval

The underwriter makes the call: approve, reject, or conditionally approve. Conditional approvals in particular require careful tracking, since they often carry requirements that must be satisfied before — or shortly after — disbursement.

8. Documentation & Disbursement

Approval isn't the finish line. Agreements must be executed, compliance checks completed, and only then are funds disbursed. Every step here carries regulatory weight, and errors at this stage are costly to unwind later.

9. PDD & Sanction Condition Tracking

Post-Disbursement Documents (PDD) and sanction conditions are where many lenders quietly accumulate risk. Pending documents, mortgage creation, insurance coverage, guarantor formalities — if these aren't tracked systematically, they become liabilities that surface only when something goes wrong. A strong platform treats this as an active workflow, not a filing exercise.

10. Loan Management System (LMS)

Once the loan is live, the LMS takes over the full servicing relationship: repayment processing, demographic changes, part payments, restructuring, top-ups, foreclosure, closure, insurance settlement, demise tagging, and auto knock-off, among other functions. This is where the loan is "lived" — and where borrower experience is won or lost over the years that follow.

11. Collections Management

When EMIs fall overdue, accounts move into collections, where teams manage follow-ups, recovery actions, and — when necessary — legal escalation. Effective collections isn't just about recovery; it's about early, structured intervention that prevents a temporary lapse from becoming a permanent default.

12. Delinquency Classification

Overdue accounts are classified with precision:

- SMA-0 — 1 to 30 days past due

- SMA-1 — 31 to 60 days past due

- SMA-2 — 61 to 90 days past due

This classification isn't just internal housekeeping — it drives regulatory reporting, provisioning, and the intensity of collection response.

13. NPA Management

If delinquency isn't resolved, the account progresses through the Non-Performing Asset classifications: Substandard Asset, Doubtful Asset, and finally Loss Asset. Each stage carries distinct provisioning and regulatory implications, and requires a different operational response.

14. Recovery & Closure

Every loan reaches an endpoint — ideally normal closure, but sometimes through settlement, waiver management, legal recovery, write-off, or insurance settlement. How well a lender manages this final stage often defines its long-term asset quality and reputation.

A Lifecycle, Not a Transaction

What this journey makes clear is that lending is not a single event — it's a continuum. A loan touches sales, credit, legal, operations, compliance, and finance teams, often simultaneously, and always in sequence. Treating any one of these stages in isolation creates blind spots; treating them as a connected lifecycle creates control.

That's the philosophy behind R2S Fincore's Lending Management platform: CRM, LOS, LMS, Collections, Credit Risk, and Compliance, working together as one system — not several systems that happen to pass files to each other.

Because in lending, the difference between a good platform and a great one isn't how fast it can originate a loan. It's how intelligently it can manage that loan for the rest of its life.

See the Full Loan Lifecycle in Action

Talk to our team to see how R2S FinCore powers lending from lead to closure.

Request a Demo